Dit document heb ik ooit geschreven voor een goede kennis met interesse in de aandelenmarkten. Het vormt een basale inleiding om de aandelenmarkten in al haar mysticiteit tastbaarder te maken. Principieel moet ik elke blootstelling aan de aandelenmarkten afraden vanwege de omvangrijke risico’s. Er zijn veel specialisten die goede aanbevelingen kunnen doen omtrent jouw vermogensplanning. Wanneer je echter jouw nieuwsgierigheid niet bedwingen kunt, is de onderstaande aanpak een veilige manier om jouw investeringskeuzes te testen aan de marktrealiteit. Deze simulatie, bekend als

paper trading kan simpel worden uitgevoerd zonder lastige oefenaccounts of een aanmelding bij een broker. Dit geeft rust en bespaart hijgende telefoontjes om die eerste storting…

Mijn Beleggingsfilosofie

Beleggen kan op talloze manieren, met een veelvoud aan

instrumenten en intensiteit. De perfecte methodologie is een afweging van

talloze parameters en hoort te groeien met jouw persoonlijkheid en ervaring. Waarschijnlijk

vormt jouw beleggingshorizon de allerbelangrijkste overweging. Met andere

woorden, wanneer wil je winsten nemen en op welke frequentie wil je handelen? Ben

je op zoek naar vermogensbescherming? Of wil je bijverdienen? Bij een passieve

belegginswijze past een langere horizon, terwijl de spanne doorgaans verkort

naarmate de houding actiever wordt. Mijn voorkeur gaat uit naar de lange termijn

en ik bezie beleggingsbeslissingen graag in lijn met meerjaren-trends. Ieder

ander - en zeker beginners - zou ik eenzelfde lange horizon aanbevelen, al is

het om niet verloren te raken in de waan (koersen) van de dag. Een strategisch belegger

met een lange horizon gebruikt een beurscrash om bij te kopen, waar een

korte-termijn belegger veel geld ziet verdampen tijdens beurscrashes. Het

rendementspotentieel is moeilijker te becijferen. Al decennia struikelen

academici, experts, beleggers en handelaren welk tijdsraam het meeste rendement

oplevert. Het gros roept dat buy-and-hold

dood is en vele transacties per jaar lucratiever zijn. Echter laat Warren

Buffet het actieve handelen over aan adrenalinejunks en bouwt gestaag en

duurzaam aan zijn portefeuille, waarin hij zelfs nog posities heeft uit zijn

beginjaren (30+ jaar). De ultieme portefeuille heeft een gewogen risico-/rendementsverhouding,

welke zijn afgestemd op de persoonlijkheid (bloeddruk en levensfase) van de

belegger. De defensieve belegger kiest voor veilig en duurzaam, terwijl de

offensieve belegger kiest voor een risicovoller en kortstondigere jacht naar

hogere rendementen. Natuurlijk loopt de defensieve belegger met een ‘veilig’ en

gestaag appreciërende Unilever het volledige risico wanneer het bedrijf

failliet gaat.

De Juiste Belegging

Professionals stellen doorgaans brede portefeuilles samen

rondom specifieke thema’s, met specifieke methodieken en doelstellingen. Binnen

deze portefeuilles zullen de fondsbeheerders diverse beleggingsinstrumenten

gebruiken voor een blootstelling aan de gewenste activaklassen en geografie. Een

activaklasse (‘asset class’) staat voor de productfamilie waarin wordt belegd (vb.

vastgoed of aandelen). De som van alle mogelijke investeringsinstrumenten heet effecten

(‘securities’). Voor dit document kijk ik naar de activaklasse aandelen (‘equities’

of ’stocks’). Aandelen hebben normaliter betrekking op bedrijven. Weet dat bedrijven

voor het aantrekken en renumereren van extern kapitaal separate fondsen oprichten.

Derhalve zoek je technisch gezien het fonds Ahold N.V. en niet de rechtspersoon

Ahold (Zaandam) B.V.

Portefeuillebeheer

Het beheer van de beleggingsportefeuille is wellicht het

allerbelangrijkste voor een renderende toekomst. Ik durf zelfs te beweren dat

ieder die faalt, dit doet vanwege slechte portfoliomanagement en niet zozeer

vanwege slechte beleggingen an sich. Een portefeuille met louter rijzende

sterren kan, onder slecht beheer, leiden tot persoonlijk faillissement. Terwijl

deze twee jaar later mooie rendementen hadden kunnen opleveren. Dus als jij

faalt, doe je dit omdat je jouw ‘zetten’ niet goed beheerst (in relatie tot je

marge). Vaak hoeven we slechts de cyclus, of de dip uit te (kunnen) zitten om

hogere toppen tegemoet te zien. Ik zal alle complexiteit besparen, maar wil

graag aandacht vestigen op regel #1 binnen portfoliomanagement; diversificatie.

En diversificatie kenmerkt zich door non-correlatie. Dit betekent dat de

diverse effecten binnen de portefeuille een historische neiging moeten hebben

tot ongelijke piek-dal momenten. Het precies tegenovergesteld bewegen van 2 effecten,

duid op negatieve correlatie (-1) en is nog steeds correlatie. Een gezonde

portefeuille is gediversifieerd in meerdere dimensies, met spreiding over

activaklassen, geografische marktbediening, sectoren, bedrijfsomvang en meer. Een

wijde spreiding binnen je portefeuille zet bij neergaande koersen niet je

gehele portefeuille onder water (gedwongen noodverkopen door afgewaardeerd onderpand=’margin

call’). Als het goed is valt er in alle 4-seizoenen zowel te oogsten als te

zaaien.

De Beurs en het Aandeel

Elk beursgenoteerd bedrijf heeft een aandeelhoudersverplichting

en zal op haar corporate websites (investor relations) informatie richting

investeerders verschaffen. Bekijk deze secties en zorg dat je de relevante

informatie uitspit om een goede beleggingscase te formuleren. Ongeacht welke

informatie jij belangrijk vindt, zorg tenminste en te allen tijde dat je de

PROSPECTUS hebt gelezen! En als er geen prospectus is, kies dan voor een andere

belegging.

Koersinfo & notering @ bmwgroup.com > Investor Relations

Exact dezelfde aandelen kunnen genoteerd staan aan

verschillende beurzen (‘exchanges’). Door tijdelijke en lokale

handelsfluctuaties kunnen op verschillende beurzen geringe prijsverschillen

ontstaan. De markt zorgt in de regel voor het gelijktrekken van deze

fluctuaties (‘arbitrage’). Zowat elk ontwikkeld land heeft één of meerdere

beurzen, welke fysieke, virtuele of hybride handel kennen. De meeste van ons kennen

Nasdaq (technologie georiënteerd), het welbekende New York Stock Exchange of

onze hoogsteigen Amsterdam Stock Exchange (de oudste beurs ter wereld). Niet

elke beurs heeft dezelfde betrouwbaarheid en liquiditeit, welke direct invloed

kunnen hebben op hoe jouw order uitgevoerd wordt.

Aandeelinformatie @ bmwgroup.com > Investor Relations

Veel bedrijven hebben meerdere soorten aandelen, elk met

eigen identificatiecodes (‘ticker codes’). De beurs van thuisland biedt vaak de

hoofdnotering (‘primary exchange’). Hier is de handel veelal het meest liquide,

hetgeen gunstig is voor de aan-/verkoopbaarheid alsook de spread (verschil

bied-laatprijs). Moderne handelsplatformen dirigeren orders automatisch naar de

beurs met de gunstigste condities.

Marktdata

Bloomberg (VS) en Reuters (Europa) zijn de marktstandaard

betreft informatieverschaffing binnen de financiële wereld. Zij bieden specialistische

gereedschappen aan professionele marktpartijen en vormen een goed vertrekpunt

voor de thuisbelegger (‘retail investor’).

Zoek direct op bedrijfsnaam of op ticker symbol. In sommige

gevallen is koersdata beschikbaar over het aandeel op meerdere beurzen. Het

meest complete beeld kan vaak gewonnen worden door de bovenste optie te

selecteren.

Effecten selectiescherm @ Reuters.com

Het goed inspecteren van deze sites op jouw

voorkeursbedrijven is werkelijk een must. Klik rond en kijk wat jij belangrijk

zou kunnen vinden (en leer).

Aandeleninformatie @ Reuters.com

Fundamentele Analyse

Het nauwgezet onderzoek naar de (financiële) onderbouwing van

markt en bedrijf staat bekend als Fundamentele Analyse. Deze analysevorm dient

inzicht te verschaffen in het vermogen van een bedrijf om waarde te vangen, te

leveren en af te zetten. Deze analyse richt zich derhalve op het bedrijf

(aanbodzijde), met als doel om onderbenutte intrinsieke waarde bloot te leggen,

maar ook op de markt als geheel (vraagzijde). Vervolgens moeten verkregen

inzichten op realistische wijze worden geëxtrapoleerd naar de toekomst, met een

gevoel voor marktontwikkeling, danwel consumententrends. Fundamentele Analyse

is omvangrijk, maar evenzo belangrijk. Het uitvoeren van de goede fundamentele

analyse en het wegen van de juiste metrieken mag jouw eerste stap naar zelfstudie

zijn.

Om je voort te helpen, kunnen we deze stelregels van meester

Buffet in ogenschouw nemen;

- Wees de directeur van het bedrijf dat je analyseert en leer JOUW bedrijf kennen (nauwgezetheid).

- Overtuigd jezelf van het bedrijf en toekomstperspectieven in die mate dat je zelfs bereid zou zijn om jouw laatste € in het bedrijf te steken. (overtuiging)

- Een goede belegger (‘investor’) houdt niet van onzekerheden. (realisme)

Technische Analyse

De fundamentele analyse heeft inzicht verschaft in onderbenutte

waarde in het verdienmodel c.q.

bedrijf. Daarna volgt de technische analyse om (een) verstandig(e) instapmoment(en)

te bepalen. We gaan naar de grafieken kijken, met andere woorden de prijs van het effect. Onthoudt dat

waarde versloten ligt in het bedrijf, terwijl de prijs slechts in de hoofden

van de observatoren (de markt) bestaat.

Welnu, tijd voor actie. Ik zal aan de hand van aandelen

enkele voorbeelden doorlopen, zodat je vervolgens in Google Finance een

fictieve portefeuille kunt opbouwen. Het samenstellen van een portefeuille kan met

diverse tools, echter prefereer ik Google. De interface is licht/snel, het

overzicht is goed, het combineert handig met het Google Account en het brengt

mij een goed overzicht van relevant en actueel nieuws rondom de betreffende

aandelen.

Google Finance

Vul in het zoekveld de bedrijfsnaam of de ticker symbol in. Google

Finance registreert maar een beperkt aantal beurzen, ETR staat in dit geval

voor de XETRA, welke de handelsplaats is van de Frankfurt Stock Exchange (hoofdnotering).

Zoek Aandeel @ Google Finance

Indicatoren en Visuele Analyse

Vanuit de Technische Analyse kijk je louter naar koersen. Deze

discipline beschouwd huidige marktprijs als de som van al het beschikbare nieuws

en marktdynamiek. Dit is natuurlijk een voortschrijdend verhaal (lees: koersverloop).

Begin ALTIJD vanuit het langetermijnbeeld voor overzicht over het strijdveld en

het relativeren van de huidige marktprijs. Visuele analyse is één. Vervolgens

maken Technisch Analisten veelvuldig gebruik van technische indicatoren. Als

voorbeeld raad ik je aan om onder de grafiek ‘technicals’ aan de te klikken en

EMA(200) te activeren. Dit is het lange-termijn (200-daags) slepend gemiddelde,

welke ik bezie als een soort ‘fair value’. Duikelen we onder dit gemiddelde,

beschouw ik het effect als ‘goedkoop’ en een beweging boven het gemiddelde

beschouw ik als ‘duur’. Daarnaast verklappen koersbewegingen onder deze

hulplijn een dalende trend en koersbewegingen erboven onthullen een stijgende

trend. Begrijp dat dit niets zegt over de (on)aantrekkelijkheid van een

aandeel. Immers had een koop in 2010, boven de EMA(200), over de jaren zeer

lucratief kunnen zijn. Klik eens wat rond en ga zelf het experiment (en

zelfstudie) aan.

Voeg Technische Indicator toe @ Google Finance

Enkele tips vooraleer je het in-/uitstapmoment bepaald:

- De trend (stijgend/dalend) is wat altijd wat het is, totdat het tegendeel bewezen is.

- Een markt die niet stijgt, daalt.

- Markten kunnen voor aanzienlijke tijd over- of onderprijst blijven.

- Bevecht al jouw aannames. En de aanname onder deze aannames.

- Wees berekend op jouw ongelijk.

En ja, deze tips klinken als peuterwijsheid. Maar er komt

een dag dat je terugdenkt aan wat hier geschreven staat…

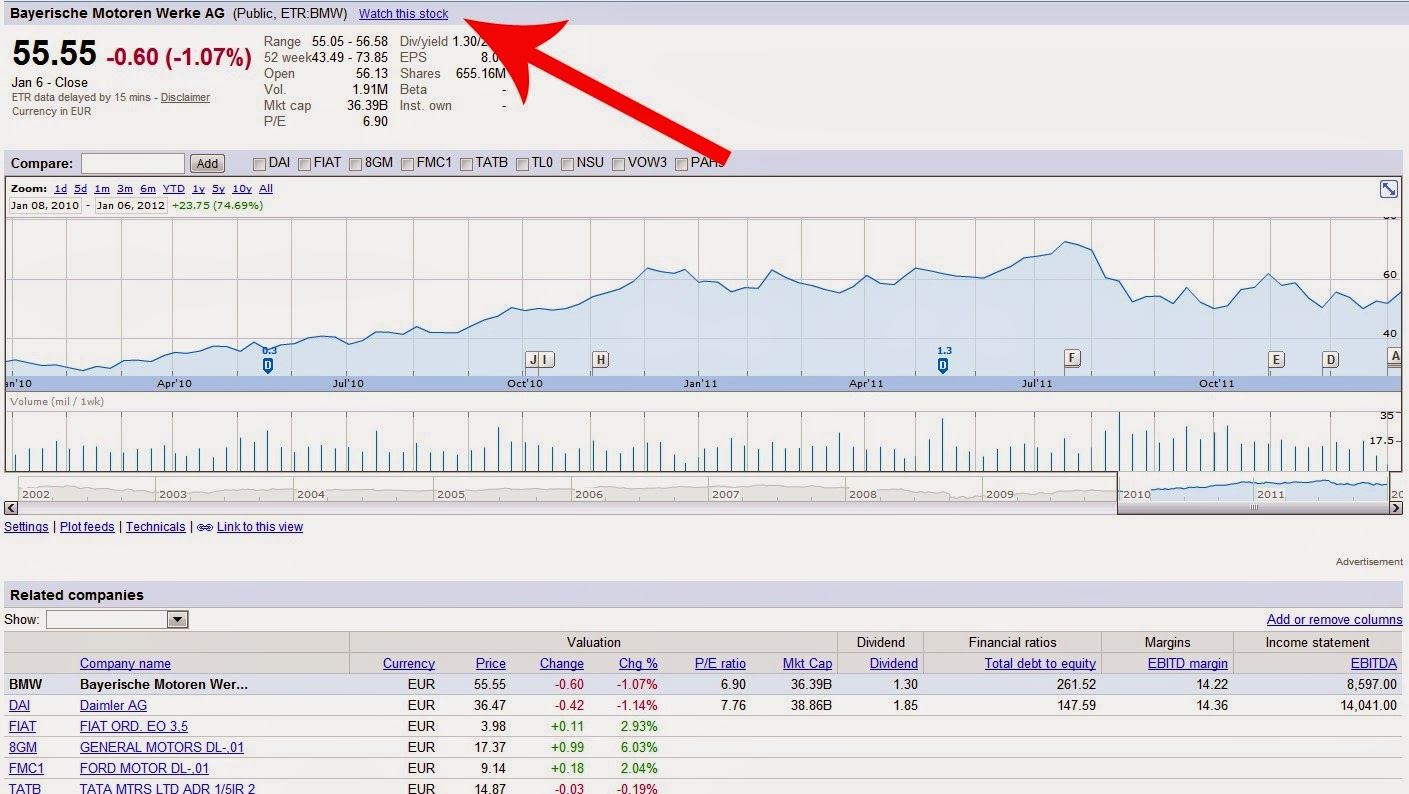

Bouw Jouw Portefeuille

Speel, kijk en vergelijk. Wat zijn de historische

aandelenkoersen, hoe hoog is het dividend en hoe verhoudt dit bedrijf zich tot

branchegenoten? Vergeet het nieuws niet te bekijken/bij te houden. Wanneer je

dit bedrijf wilt toevoegen aan je watchlist kies je Watch this stock.

Assembleer jouw shortlist @ Google Finance

Onder My Portfolio

bevindt zich de persoonlijke watchlist, voor een snel overzicht van alle, als

interessant gemarkeerde effecten. Deze watchlist bouw je gemakkelijk om tot een

volwaardige beleggingsportefeuille, door het toevoegen van transacties.

Portefeuille Transacties en Prestaties @ Google Finance

- Hier vind je de resultaten van de geselecteerde aandelen, al dan niet met persoonlijke winst-/verlies gegevens (alleen indien er transacties zijn toegevoegd).

- Hier kun je transacties toevoegen, ook in het verleden.

- Vergeet niet om de valuta op de €uro te zetten

Belangrijke Toevoegingen

Valutarisico

Indien je aandelen op buitenlandse beurzen koopt, reken je

deze ook af in de valuta in kwestie. Deze valutatransacties gaan gepaard met

variaties in euro/dollar-koers. Tevens kunnen voor deze muntconversie extra

transactiekosten gerekend worden. Ook zal er, indien er nog geen Dollars in

bezit waren, automatisch een rentedragende lening gesloten worden.

Transactiekosten

De transactiekosten moeten ook meegenomen worden (en kunnen

in Google Finance worden toegevoegd). Bereken de kosten op basis van commissie

over de totale transactiewaarde.

Kopen is 1 transactie,

maar verkopen (voor winstnemingen) is nog 1 transactie...

Margin Account

Rood staan kost geld. Met een klein beetje gemak handel je

al onder hefboom. Dit speelt niet mee in je Google-account, maar wel in een echte

omgeving. Het hiermee omgaan voegt een hele nieuwe dimensie aan het

(portefeuille)beheer toe. Wanneer de onderpand zakt, is een groter component

van jouw dekking onder nieuwe aankopen ingeleend (vreemd vermogen). Wanneer je echt gaat beleggen is het van vitaal belang dit mechanisme goed te begrijpen, of absoluut NIET met hefboom ('on margin') te handelen.

Oh, en mocht je initieel succes boeken (waarschijnlijk geluk

en omdat de koers is gestegen om redenen die jij echt niet doorziet) en de Tony

Montana in jou de overhand neemt;

Behaalde resultaten uit het verleden, bieden geen garantie

voor de toekomst.

Enkele links

Investopedia is een waardevolle bron voor kennisverbreding omtrent beleggen. Zij bieden een simulator in een gesloten omgeving, waar je een gevoel kunt krijgen voor handel MET een beperkte portemonnaie. Ik heb geen ervaring met de tool, maar het kan interessant zijn.

Alle in dit document genoemde voorbeelden vormen geen

beleggingsadvies. De specifieke voorbeelden zijn louter bedoeld ter

illustratie.

{kind=link}